- https://www.indiacode.nic.in/bitstream/123456789/1988/1/A1999_42.pdf

- https://incometaxindia.gov.in/forms/income-tax%20rules/103120000000007842.pdf

- https://incometaxindia.gov.in/forms/income-tax%20rules/103120000000007944.pdf

Table of Contents

What is an NRE Account?What Is an NRO Account?NRE vs NRO Account â Detailed Comparison TableTaxation on NRE vs NRO AccountsDifference Between NRE and NRO Bank AccountRepatriation Rules for NRE and NRO AccountsStep-by-Step Repatriation Process (NRO Account)Documents Required for NRE & NRO AccountsNRE or NRO â Which Account Should You Choose?Real-Life Use CasesCan NRIs Have Both NRE and NRO Accounts?Conclusion

Loved what you read? Share it with others!

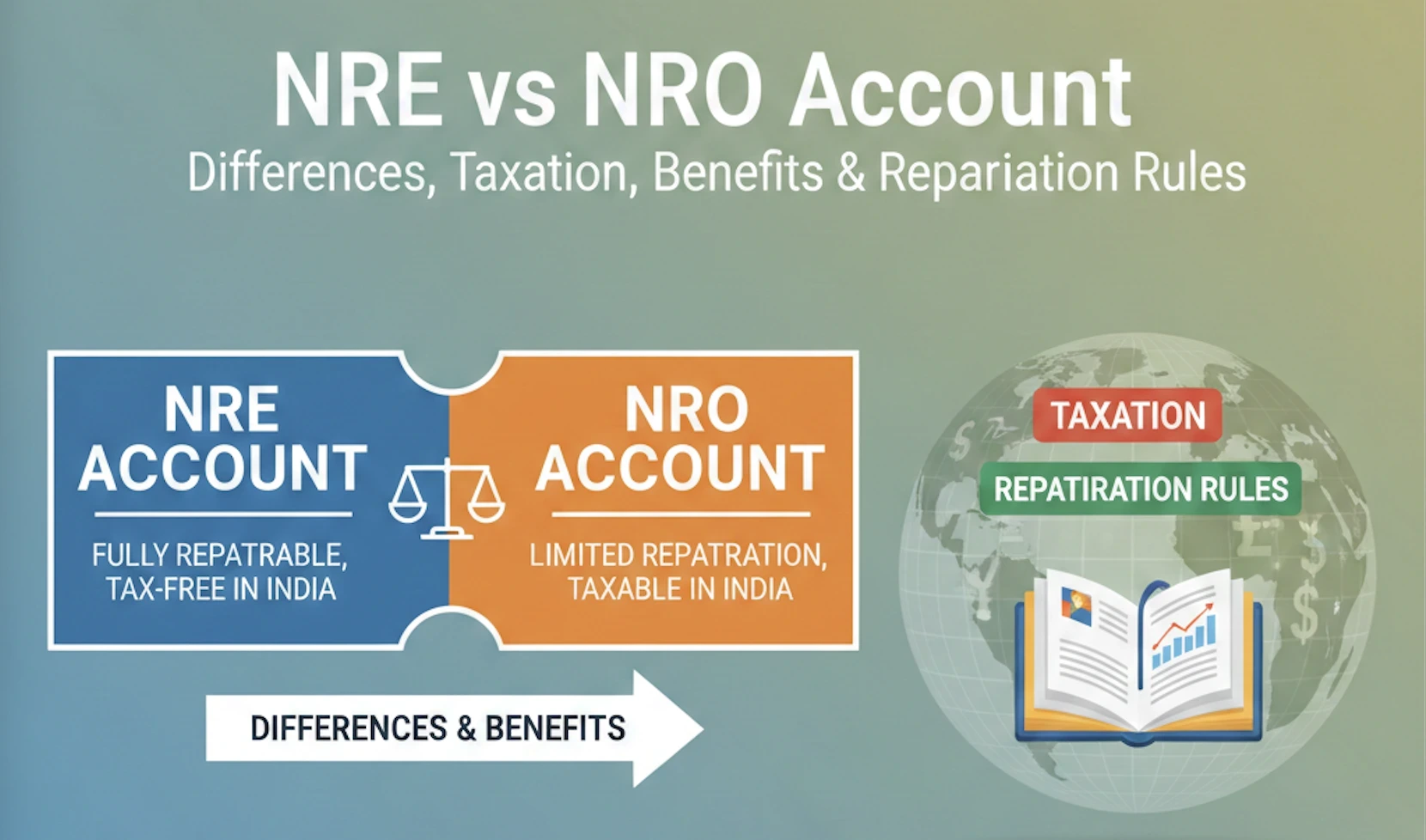

NRE vs NRO Account: Differences, Taxation, Benefits & Repatriation Rules

Updated : February 17, 2026, 11:40 AM

Author :

![]() Suju

Suju

Summary

Understanding the NRE vs NRO account helps NRIs manage money from abroad and India efficiently. An NRE account is ideal for foreign income, offers tax free interest and allows full repatriation. An NRO account is for Indian income, earns taxable interest and allows limited repatriation. Both account are maintained in INR. NRIs can hold bold accounts to save on taxes, move funds securely and manage money while staying compliant with Indian banking rules.

Table of Contents

What is an NRE Account?What Is an NRO Account?NRE vs NRO Account â Detailed Comparison TableTaxation on NRE vs NRO AccountsDifference Between NRE and NRO Bank AccountRepatriation Rules for NRE and NRO AccountsStep-by-Step Repatriation Process (NRO Account)Documents Required for NRE & NRO AccountsNRE or NRO â Which Account Should You Choose?Real-Life Use CasesCan NRIs Have Both NRE and NRO Accounts?Conclusion

NRE vs. NRO accounts often confuse NRIs handling cross-border transactions. Non-Resident External (NRE) accounts are for foreign income, such as overseas salary, and allow full repatriation. Non-Resident Ordinary (NRO) accounts are intended for Indian-source income, such as rent, pensions, or property income. Tax implications matter because NRE interest is tax-free, while NRO interest is taxable in India. For example, foreign salary should be in NRE, but rent from an Indian property must go into NRO. Understanding these differences ensures compliance, smooth transfers, and better financial planning, without confusion or costly mistakes, for NRIs globally.

What is an NRE Account?

NRE accounts are bank accounts for NRIs to hold foreign income in India, offering tax-free interest, full repatriation, and secure, compliant management of overseas earnings.

Key Features of an NRE Account

- Indian income handling: NRE accounts are primarily for foreign income; Indian income cannot be deposited.

- Currency conversion: Funds are deposited in foreign currency and maintained in Indian rupees.

- Tax applicability: Interest earnings: Both principal and interest may be freely repatriated without tax on an NRE account, which is completely tax-free in India.

- Repatriation limits: Both principal and interest may be freely repatriated without limit.

Who Should Use an NRE Account?

NRIs with foreign-sourced salaries, overseas business income, or long-term investment plans in India can benefit from an NRE account. It safely holds foreign earnings, earns tax-free interest and allows easy repatriation, making money management simple and stress-free.

What Is an NRO Account?

An NRO account helps NRIs manage income earned in India, such as rent or dividends, and enables local payments and deposits while residing abroad, in compliance with applicable Indian banking laws.

Key Features of an NRO Account

- Indian income handling: NRO accounts are used to manage income earned in India, such as rent, pensions, and dividends.

- Currency conversion: Funds can be deposited in Indian rupees or foreign currency, but are maintained in rupees.

- Tax applicability: Interest earned on NRO accounts is taxable in India under applicable income tax laws.

- Repatriation Limits: Repatriation is permitted up to USD 1 million per financial year, subject to tax compliance.

Who Should Use an NRO Account?

NRIs earning rental income, receiving property sale proceeds, or collecting a pension are dividends in India should use an NRO account. It helps manage Indian income securely, pay local taxes, and handle routine expenses. While repatriation is limited, it ensures compliance with Indian regulations and simplifies the receipt and use of funds earned in India.

NRE vs NRO Account – Detailed Comparison Table

This table compares NRE and NRO accounts, highlighting key differences in income types, taxation, repatriation, and the benefits of NRIs.

| Feature | NRE Account | NRO Account |

| Income Source | Foreign income | Indian income |

| Currency | INR | INR |

| Interest Tax | Tax-free | Taxable |

| TDS | No | Yes |

| Repatriation | Fully allowed | Limited |

| Joint Account | NRI allowed | NRI + Resident allowed |

| Best For | Overseas earnings | India-based income |

Taxation on NRE vs NRO Accounts

Understanding the taxation of NRE & NRO accounts is vital for NRIs. NRE interest is tax-free, while the NRO account taxation rules apply to interest earned, rental income, and property proceeds in India, ensuring compliance and proper financial planning.

Is NRE Account Interest Taxable?

Interest earned on an NRE account is completely tax-free under Indian tax law, has no TDS deduction, and is fully Foreign Exchange Management Act [1] (FEMA)-compliant, making it ideal for NRIs to safely earn and repatriate foreign income.

How Is NRO Account Interest Taxed?

Interest on an NRO account is taxed according to the applicable Indian income slab, with TDS deducted at source. NRIs may reduce their tax liability under the DTAA.

Mini Example Block:

₹5,00,000 interest in NRO account → TDS applied → DTAA benefit may lower overall tax.

Difference Between NRE and NRO Bank Account

Below is a simple guide that highlights the difference between NRE & NRO accounts to help NRIs easily understand taxation, repatriation, deposits, withdrawals, and fund management in India.

| Feature | NRE Account | NRO Account |

| Purpose | Hold foreign income | Manages income earned in India (rent, pension, dividends) |

| Tax on Interest | Tax-free | Taxable as per the income slab |

| Repatriation | Fully repatriable | Limited to USD 1 million/ year after tax |

| Deposits & Withdraws | Only foreign currency allowed | Indian or foreign currency allowed |

| Fund transfer | Freely transferable to India/abroad | Transfer mainly within India; limited abroad |

| Currency | Maintained in INR | Maintained in INR |

| Account holders | NRIs only | NRI & PIOs |

| Joint Account | Can be held with another NRI only | Can be held with another NRI or resident Indian (former or survivor basis) |

Repatriation Rules for NRE and NRO Accounts

Repatriation rules explain how NRIs can transfer money from India abroad. NRE allows full repatriation, while NRO permits limited tax-adjusted transfers, helping manage foreign earnings and Indian income efficiently.

NRE Account Repatriation Rules

In an NRE account, both interest and principal are fully repatriable with no limits. This allows NRIs to freely transfer their foreign earnings from India at any time, ensuring complete financial flexibility.

NRO Account Repatriation Rules

NRIs can transfer Indian income abroad through NRO accounts, but repatriation is limited, and tax compliance and required documentation are required for smooth processing.

- Annual limit: Funds can be repatriated up to USD 1 million per financial year.

- Required forms: Submission of Form 15CA/15CB [2] is mandatory for repatriation.

- Tax clearance needed: Taxes must be paid on interest and Indian income before transferring funds abroad

Step-by-Step Repatriation Process (NRO Account)

Repatriating funds from an NRO account requires tax compliance, form submission, bank verification, and transfer to your overseas account. Below is the step-by-step process:

- Ensure Tax Payments TDS: Pay applicable taxes on interest or income, and ensure TDS is deducted in accordance with Indian rules.

- Submit required forms: Complete Form 15CA and get Form 15CB from a chartered accountant for tax compliance.

- Bank Verification: Submit the form to your bank. The bank verifies tax payments and documents.

- Transfer to Overseas account: Once approved, the bank transfers the funds abroad within the permissible annual limit.

Documents Required for NRE & NRO Accounts

NRIs need specific documents to open NRE or NRO accounts in India. These verify identity, address and NRI status, ensuring smooth account opening and regulatory compliance.

Documents to Open an NRE Account

- Passport: Valid passport as proof of identity

- Visa/work permit/OCI card: Proof of NRI status

- Overseas address proof: Utility bills, rental agreement, or bank statement.

- Photographs: Recent passport-sized photos.

- PAN Card/ Form 60 [3]: For tax identification in India.

- Bank reference letter (optional): From your overseas bank to simplify verification.

Documents to Open an NRO Account

- Passport: Valid passport as proof of identity.

- VISA/OCI/PIO Card: Proof of NRI or PIO status.

- Indian address proof: Aadhaar, voter ID, or utility bills (if available)

- Photograph: Recent passport-size photograph.

- PAN Card/ Form 60: Required for tax purposes in India.

- Income proof (optional): For some banks, to verify the source of Indian income.

NRE or NRO – Which Account Should You Choose?

Choose an NRE account if you earn abroad and want tax-free interest with full repatriation. Use an NRO account for Indian income, with NRO taxation and repatriation limits in mind to ensure compliance.

Choose NRE If:

If most of your income comes from outside India, an NRE account is ideal. It gives you tax-free interest, meaning your earnings grow without being taxed in India. It offers easy repatriation, so you can transfer both principal and interest back to your home country at any time, making it simple to manage your money across countries.

Choose NRO If:

If you earn income in India, like rental payments or property sale proceeds, an NRO account is suitable. It’s also useful if you receive a pension or dividends and want to manage Indian expenses such as bills, taxes, or maintenance. This account helps you keep all your Indian earnings organised while staying compliant with Indian tax rules. Though repatriation is limited, it ensures safe, easy handling of funds within India.

Real-Life Use Cases

Below are practical examples showing when NRIs should use NRE or NRO accounts to simplify money management and ensure tax compliance.

Scenario 1 – NRI Earning Salary Abroad

If you work overseas and receive your salary in a foreign bank, an NRE account is ideal. It allows you to deposit your foreign earnings in India, earn tax-free interest, and transfer money back abroad anytime. This keeps income secure, accessible, and fully repatriable with no hassle.

Scenario 2 – NRI Renting Property in India

If you own property in India and earn rental income, an NRO account is the best option. It allows you to deposit rent securely, pay applicable taxes, and manage Indian expenses such as maintenance, property taxes, and bills. While repatriation is limited to USD 1 million per year, it ensures compliance with NRO taxation rules, making it easy and legal to handle all income generated from your Indian property.

Scenario 3 – NRI Selling Property in India

If you sell property in India, the sale proceeds must be deposited in an NRO account. Taxes must be paid, and proper documentation must be completed. Up to USD 1 million can be repatriated yearly. This ensures compliance with NRO tax rules and the safe transfer of funds abroad.

Can NRIs Have Both NRE and NRO Accounts?

Yes, NRIs can legally hold both NRE & NRO accounts. Having both is smart because NRE handles foreign income with NRE taxation benefits, while NRO handles Indian earnings, such as rent or dividends. Using both together helps efficiently separate funds, simplify tax compliance and plan repatriation, making financial management easier and fully compliant with Indian regulations.

Common Mistakes NRIs Make

Many NRIs unknowingly make banking mistakes that lead to tax issues, penalties, or repatriation problems later while managing money abroad.

- Using a savings account instead of an NRO: Indian income, like rent, must go into an NRO, not a regular savings account.

- Ignoring TDS on NRO: Not accounting for TDS can cause tax shortfalls and compliance issues.

- Wrong account for rental income: Rental or property income should never be deposited in an NRE account.

- Missing DTAA benefits: Failing to claim DTAA can result in paying higher tax than required.

Conclusion

NRE & NRO accounts help NRIs manage foreign and Indian income smoothly while staying compliant with Indian regulations. Choosing the right account avoids tax issues and simplifies repatriation. NoBroker helps NRIs with account selection, tax guidance, repatriation support, and end-to-end financial services, making banking, investments and compliance easy, secure, and stress-free from anywhere in the world.

Is the NRE account completely tax-free?

Yes, NRE account interest is fully tax-free in India, with no TDS, but foreign country tax rules may apply there.

Can I transfer money from NRO to NRE?

Yes, funds can be transferred from NRO to NRE after paying taxes and completing all required documentation and compliance formalities.

What happens if my NRI status changes?

If NRI status changes to resident, NRE & NRO accounts must be converted to resident accounts immediately, in accordance with the rules.

Can residents be joint holders in an NRE account?

Residents can be joint holders in NRE accounts only on a former or survivor basis, without operational rights during the account lifetime.

Do I need to file a tax return for NRO interest?

Yes, filing a tax return is required if NRO interest is taxable, even when TDS has been deducted under Indian law.

ARTICLE SOURCES

Most Viewed Articles

NRI Power of Attorney for Property in India: How to Apply, Documents Required and Format

June 1, 2025

31392+ views

Know About ICICI NRI Account: Document Required, Eligibility and Application Process in 2026

January 31, 2025

27237+ views

NRI Accounts in India: List of Best NRE, NRO & FCNR Accounts in 2026

June 1, 2025

18254+ views

NRE vs NRO Account: Differences, Taxation, Benefits & Repatriation Rules

January 31, 2025

10057+ views

TDS on Sale of Property by NRI: 2026 Tax Rates, Rules & Process

June 1, 2025

9815+ views

Author

Author

Loved what you read? Share it with others!

Recent blogs in

NRI Rights in India for Property: Ownership, Inheritance & Legal Rules for 2026

November 21, 2025 by Vivek Mishra

What is NRI Certificate: Meaning, Uses, Documents Required & Procedure in India

August 25, 2025 by Vivek Mishra

Power of Attorney from UAE to India: Format, Documents & Legal Process in 2026

August 25, 2025 by Vivek Mishra

Power of Attorney for India Property from UK: Format, Documents & Legal Process in 2026

August 25, 2025 by Vivek Mishra

DTAA Between India And France: Tax Relief, TDS Rules & Benefits in 2026

August 22, 2025 by Kruthi

Full RM + FRM support

Full RM + FRM support

Join the conversation!